Wildfires Ignited in the Carolinas After Subsiding in California

Not long after the infernos blazing in California reached containment a few weeks ago, new fires have now erupted in the Carolinas. Officials listed more than 200 fires last week across North Carolina [1]. One blaze in Polk County (the Melrose fire), located in western North Carolina, was by far the largest wildfire in the state’s history [1]. In South Carolina, a fire just outside of Myrtle Beach was also the largest in the state’s history [1]. The blaze located in North Carolina was on the fringes of the area badly affected by Hurricane Helene [2]. Fallen trees and debris that have not been cleared were increasing the risk of fire throughout the state. In South Carolina, hundreds of years of decomposing vegetation created peat, which can burn for a long time when it dries out [2]. This resulted in one of the most dangerous fire situations in South Carolina.

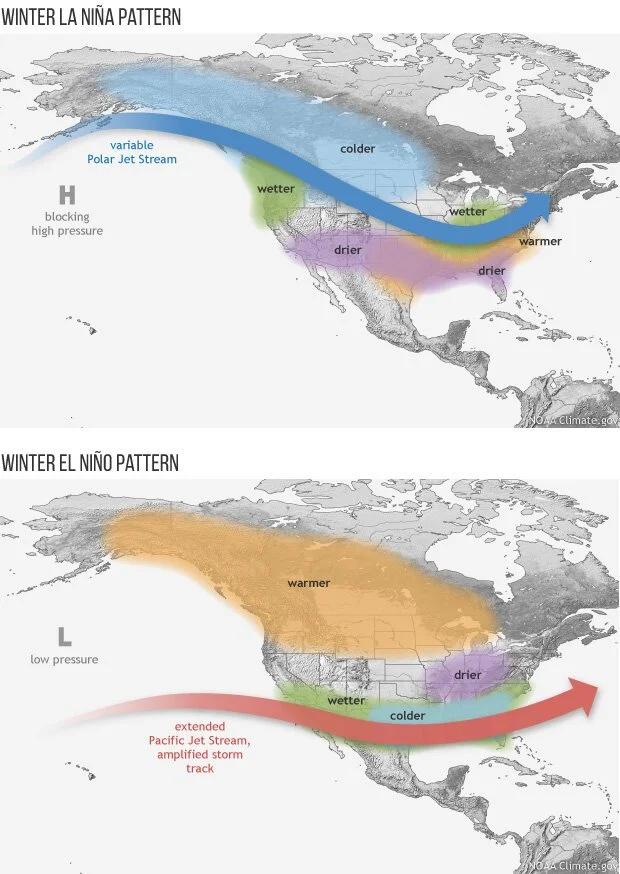

What was the trigger event? A drier-than-normal winter across the Carolinas, partly attributed to La Niña in the equatorial Pacific, combined with high winds and low relative humidity as a cold front passed through [2]. This cold front lacked the usual precipitation that accompanies these systems in this region. The fire outside of Myrtle Beach was linked to a South Carolina woman’s backyard, and she is now facing charges [3]. As for the other fires, it is very likely that this preceding weather system provided a spark. Fortunately, weakening winds provided sufficient relief in recent days, allowing firefighters to get the situation under control relatively quickly [3].

The fires in California are estimated to have caused tens of billions of dollars’ worth of damage. While the damage from fires in the Carolinas doesn’t approach that in California, fire danger is growing in many locations from a combination of factors including climate change and the increase in exposure due escalating population and property values. These factors combined with an impending insurance crisis in some states prompts us to ask how we can better model these extreme events to save lives and property and implement actions to mitigate wildfire risk.

What do We Need to Model Wildfire Risk?

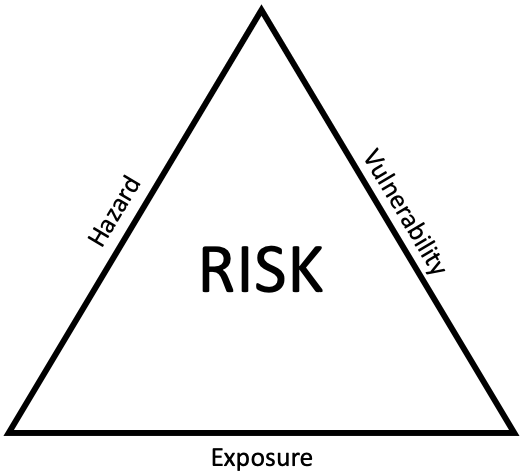

Just like with tropical cyclones, scientists use catastrophe risk models to simulate the hazards and impacts from wildfires. There are three main components to any catastrophe risk model: hazard, damage and loss [4]. The hazard module simulates wildfire occurrence, spread, and intensity based on climate conditions, topography, and vegetation. The damage module estimates how structures and properties are affected by wildfires. And lastly, the loss module quantifies financial losses for insurers, incorporating property damage and business interruption costs. The latter two components are also sometimes called exposure and vulnerability, respectively [5] (see Figure 1). The accuracy of these models largely depends on historical data that is normalized for inflation, population changes, and property values [4].

Figure 1: Crichton risk triangle (coined by David Chrichton) associated with a natural disaster [4]. Risk can be defined as a composite of the hazard, exposure, and vulnerability associated with an event. If any of the three factors is magnified, then the total risk increases, sometimes nonlinearly.

There are several factors that influence wildfire risk. The first is natural climate variability, driven by cycles such as the El Niño-Southern Oscillation (ENSO) and the Pacific Decadal Oscillation (PDO), which influence patterns of temperature and precipitation on seasonal to annual time scales [4, 6]. In addition, seasonal events such as the Santa Ana winds in California can exacerbate fire spread and intensity—this was a primary driver of the large wildfires that incinerated California back in January [4, 7]. Furthermore, there has been a historical suppression in the number of controlled burns that have occurred in the western United States in recent years, which has led to a buildup of fuel, making fires more intense when they do occur [4]. Population growth and further development also worsen the impacts, as increasing exposure leads to greater economic and property losses from wildfires. Proper land management, such as controlled burns and clearing vegetation, are imperative for mitigating wildfire risks. Property types also play a role, as homes with fire-resistant materials and cleared vegetation have a much higher chance of surviving wildfires.

Make it stand out

Figure 2: Winter La Niña pattern (top) vs. Winter El Niño pattern (bottom) and the effects on the jet stream and precipitation patterns. El Niño generally results in storm tracks farther south, which could enhance rainfall in Southern California and the Southwestern USA. Conversely, La Niña generally leads to storm tracks farther north, enhancing precipitation across the Pacific Northwest. Source: https://www.climate.gov/news-features/blogs/enso/changes-enso-impacts-warming-world

Implications for Insurers

With all this in mind, what are the implications to insurers? For one, many insurance companies have moved away from relying purely on historical loss data to estimate the impacts of wildfires [4]. The most common approach employs the use of catastrophe models that integrate climate, land use, and fire behavior data [8]. Existing risk models also need to be continually updated to reflect existing and long-term trends, including climate change and increased exposure/economic development [8]. There remains a great need for standardized data collection on wildfire losses to improve the accuracy of these models [4].

References

1. https://www.cbsnews.com/news/carolina-fires-map-where-wildfires-burn-2025/

3. https://edition.cnn.com/2025/03/09/us/south-carolina-fire-cause-myrtle-beach/index.html

5. https://www.ilankelman.org/crichton/1999risktriangle.pdf

6. https://www.climate.gov/news-features/blogs/enso/changes-enso-impacts-warming-world

7. https://www.bbc.com/weather/articles/cg7r7rrex8no

8. https://www.casact.org/sites/default/files/2022-10/RP_Cat_Models_for_Wildfire_Mitigation.pdf

9. https://www.mdpi.com/2571-6255/2/2/30

10. https://www.gov.ca.gov/2025/01/13/california-forest-management-hotter-drier-climate

11. https://fireecology.springeropen.com/articles/10.4996/fireecology.0302003